Sue Mitchell

October 3 2018

AFR

Coles’ margins will fall following its demerger from Wesfarmers and margins in food, liquor and convenience/fuel will undershoot those at Woolworths, giving the new management team plenty of room for improvement.

According to analysis by JP Morgan analyst Shaun Cousins, Coles’ total earnings before interest and tax will fall from a reported $1.5 billion in 2018 to $1.49 billon in 2019, with $55 million in new corporate overheads and self-insurance costs offsetting improved underlying earnings from supermarkets, liquor and convenience.

JP Morgan estimates Coles’ group margin in 2019 after the demerger will be around 3.7 per cent, compared with 3.8 per cent in 2018, before the new overheads.

Woolworths’ Australian food, liquor and convenience/petrol businesses earned $2.44 billion in 2018 on sales of $50 billion, an EBIT margin of 4.8 per cent. However, direct comparisons are difficult because the margin figure excludes Woolworths group central overheads of $136 million (which includes costs for other businesses including BIG W, New Zealand supermarkets and hotels).

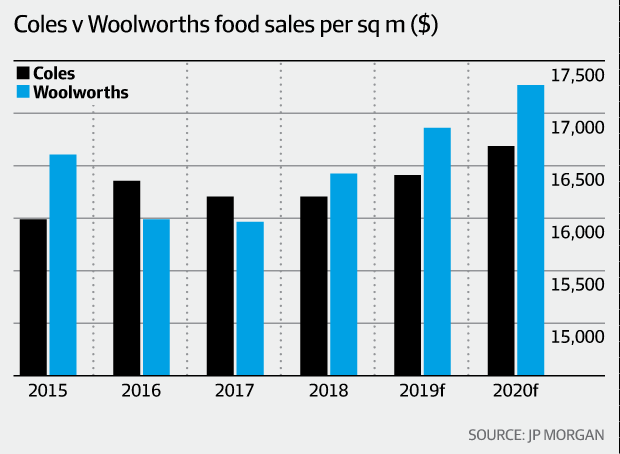

On a like-for-like basis, before taking into account corporate overheads, Mr Cousins expects Coles’ supermarkets to earn 4.17 per cent in 2019 compared with 4.6 per cent at Woolworths Australian supermarkets.

This reflects Coles’ smaller scale relative to Woolworths, lower sales of high-margin fresh foods and lower sales per square metre.

Competition by numbers

In liquor, JP Morgan expects Coles to earn 3.98 per cent, well below Woolworths’ Endeavour Drinks margin of 6.27 per cent. The difference reflects Coles’ smaller scale, lower levels of higher-margin private label products and smaller sales of wine.

In convenience and petrol, Mr Cousins expects Coles to earn 1.9 per cent, compared with 5.1 per cent at Woolworths’ petrol business, which is exploring a $1.8 billion trade sale or initial public offering.

Coles’ lower margin in convenience largely reflects its higher sourcing costs from supplier Viva Energy and lower sales.

Coles’ fuel and convenience sales have fallen 23 per cent over the last three years, from $7.4 billion to $5.7 billion, and earnings are estimated by JP Morgan to have fallen 19 per cent, from $136 million to $110 million, due to loss of market share under its premium-priced supply deal with Viva. Coles has been in discussions with Viva for two years to improve the terms of the supply deal.

One of the benefits of the demerger is that for the first time since Wesfarmers’ $20 billion acquisition of the Coles Group in 2007, a stand-alone Coles is expected to release more details about sales, gross margins, cost of doing business and EBIT margins for each of its businesses.

This will enable analysts and investors to better analyse and compare Coles’ performance with Woolworths.

Valuation

Mr Cousins has valued Coles at between $18.3 billion and $18.6 billion and expects it to trade at a 10 per cent discount to Woolworths.

Like most analysts, Mr Cousins expects Coles’ same-store sales growth to accelerate in the first quarter of 2019, buoyed by the successful Little Shop campaign and backflip over free plastic bags.

However, he expects Woolworths to outperform Coles over time due to superior strategy and execution, a better store network, stronger fresh-food sales and management stability.

New Coles managing director Steve Cain joined the retailer two weeks ago from Metcash and most of his senior executives are relatively new to their roles.

Wesfarmers is expected to release demerger documents for Coles in the next week.

Subscribe to our free mailing list and always be the first to receive the latest news and updates.